The daunting task of starting a budget is very off putting for many people, including us. It was an eye opener on what was happening to our finances. Even if you don’t want to follow a budget at the bare minimum at least track where your expenses are going, you may be unpleasantly surprised!

Introduction

When we first set out on our path to FIRE our budget was the first thing we looked at, creating The Gap, the difference between your income and your spendings. Alongside other key areas of focus there were two terms that really resonated with us and feel should be shared as much as possible, Pay Yourself First and Zero Based Budgeting.

Budgeting Terms

Pay Yourself First

Paying yourself first is fundamental to operating a successful budget plan. This entails any income that you receive to be paid to you, simple it seems, but here’s the catch, the amount of income that is paid to you will not be your salary instead it will be your allowable spending. The figure amount that you decide will be allocated by your budget.

Zero Based Budgeting

This is one we especially like. Zero based budgeting means at the end of all your budget allocations you will end up with zero dollars. This means every dollar will get tasked with a job whether it is paying bills, savings, investing or holiday fund. There is no question in where your funds have gone. This one goes hand in hand with the next term. The Envelope System.

Envelope System

The envelope system was coined this phrase due to becoming popular well before the digital age. It meant that somewhere in your house were envelopes and each envelope would be labelled with a purpose. This could be groceries, other bills or just savings. It ties in extremely well with zero based budgeting as each week you would withdraw your cash and allocate amounts into each envelope according to your budget. In today’s digital age this is much simpler, there are several banks out there that facilitate this function extremely easy. For example our mortgage is offset with a savings account, within the account we can open several other up to 10 more, each of these add to offsetting the mortgage. Each account can be labelled and transactions automated to fill up the accounts for each determined expenditure. When it comes time to collect simply locate the envelope with the labelled expense.

Automation

Tieing the two together, zero based budgeting and the envelope system you will have a power house budgeting strategy and never be short of funds. To increase the effectiveness further you will want to automate the transactions. Using your bank you can schedule transactions as you receive your pay and to go a step further some employers allow you to split your pay into two bank accounts, this removes any psychological barriers and allows you to remove unnecessary thoughts from your mind.

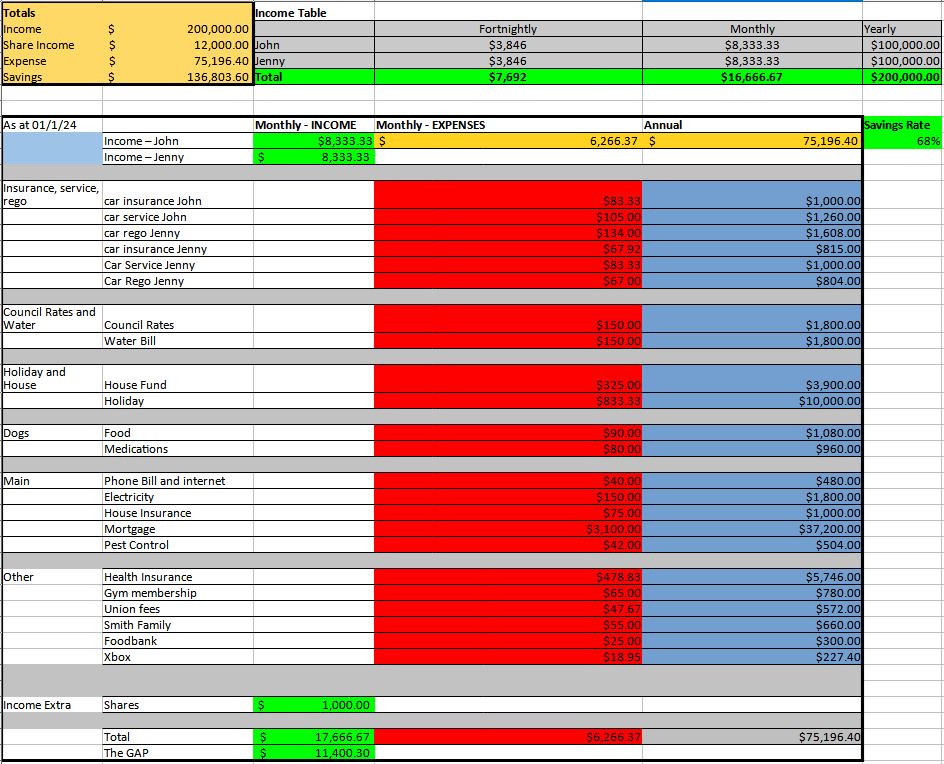

The How To

What can a budget look like? Here is an extremely simplistic view of a budget. We use this spreadsheet we made method below. Every time we get paid we have individual accounts in the left hand column, the amount is automatically deducted and placed inside it’s envelopes. The amounts in the tables are taken by a forecasted view ahead of the expense and then we add 5% for errors. So for example, an annual car registration fee of $1000 we will divide that by 12 months to get our monthly expense. All the formulas are pre-entered in the budget so each year all we need to do is add new values. If one of our envelopes ends up running out we come back to this budgeting schedule and find out why, often it will be because of a cost increase which we would simply increase the dollar amount. This allows us to pay any incoming expense without a second thought of where it is coming from.